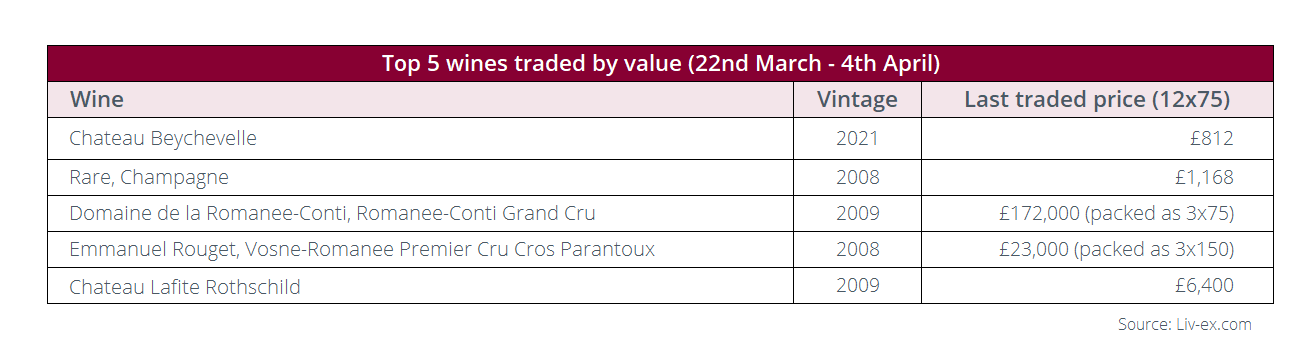

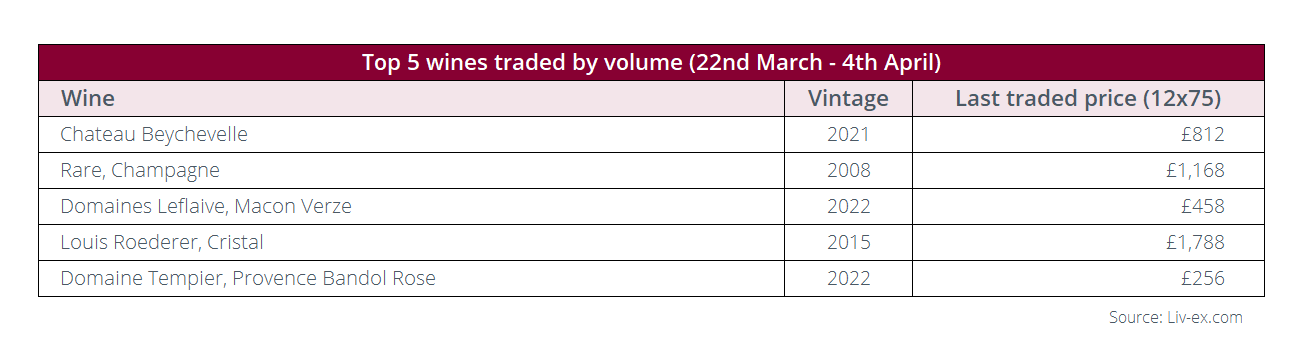

Bordeaux and Burgundy led the last two weeks of trade, followed by Champagne. Château Beychevelle 2021 was the most-traded wine both by value and volume.

What’s happening in the secondary market?

After a short break on account of the Easter Bank Holiday in the UK, this edition of Talking Trade considered the last two weeks of trade (22nd of March to the 4th of April).

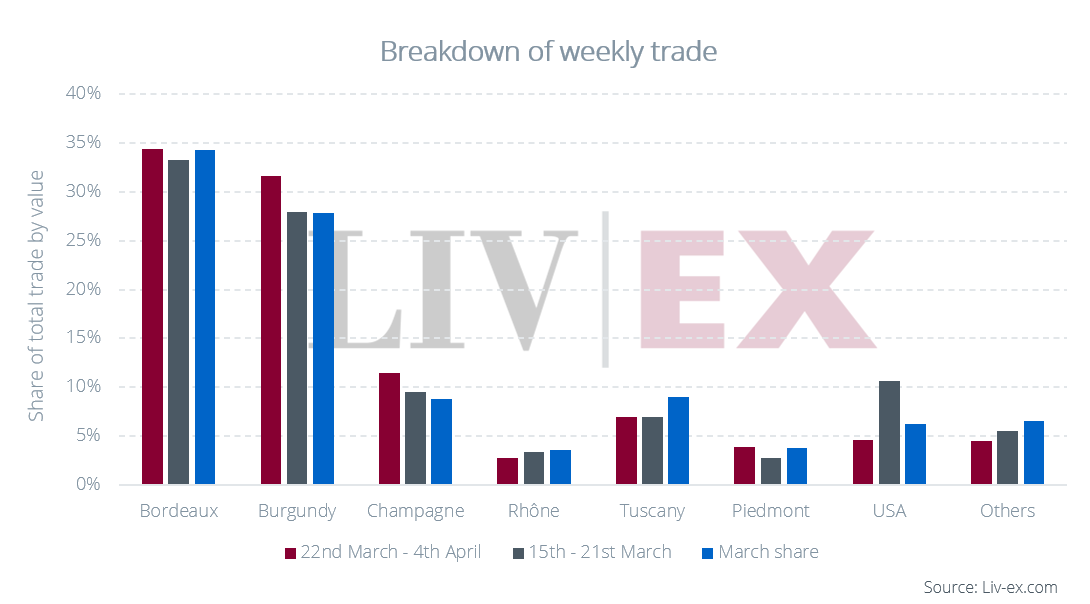

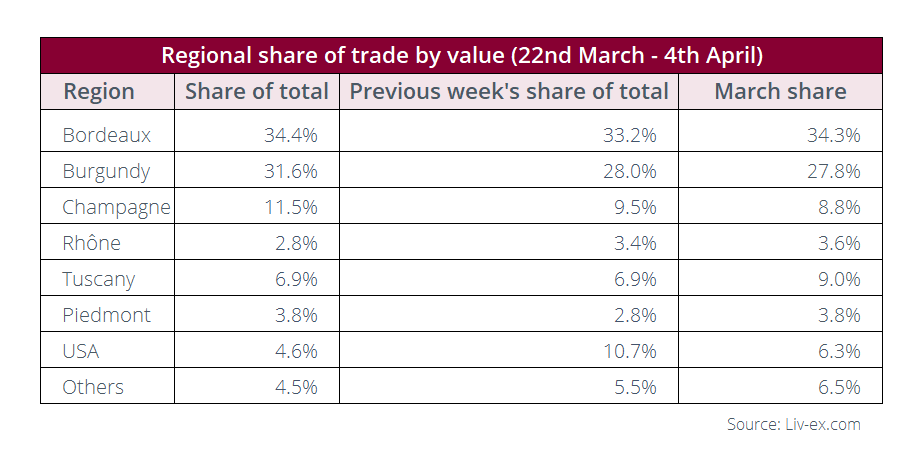

The standing at the top remained much unchanged: Bordeaux was in the lead with 34.4% of total trade by value, almost exactly matching its March trade share of 34.3%. It was followed by Burgundy, which closed the last two weeks with 31.6% of trade, up from the previous week’s 28.0%.

Champagne was also on the up, rising from 9.5% to 11.5% of total trade after the last two weeks. Two of the region’s wines featured among the most-traded wines by volume, including Rare 2008 which was the second-most traded wine by value. Piedmont recorded a modest rise from 2.8% to 3.8% of trade to equal its March trade share.

Elsewhere, the picture was less rosy. Tuscany’s trade share remained flat compared to the previous week at 6.9%, while the Rhône and the ‘Others’ category took a dip. The USA was the biggest faller, its trade share more than halving from 10.7% to 4.5% at the close of the last two weeks.

What were this week’s top-traded wines?

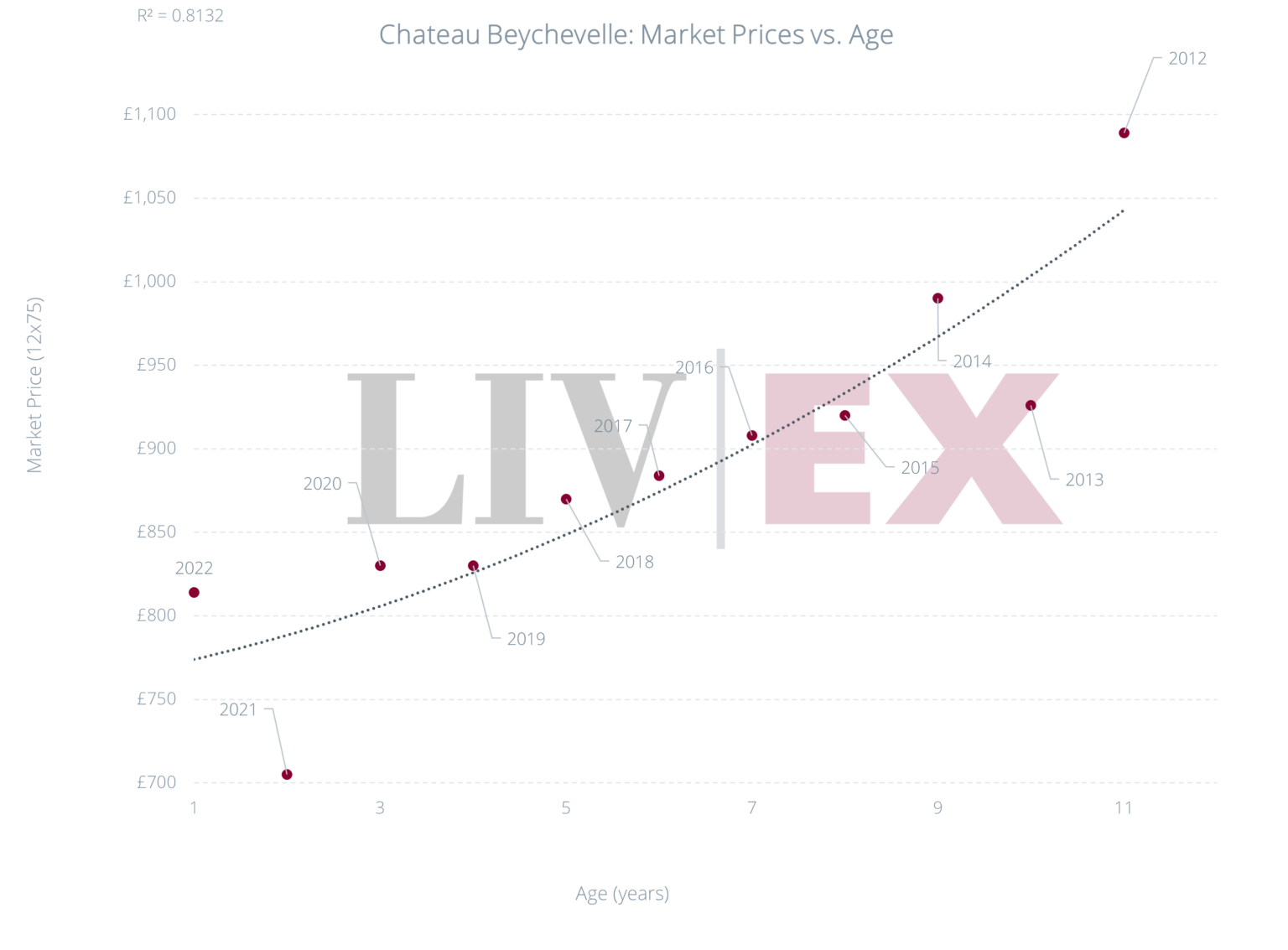

Château Beychevelle 2021, recently released in bottle, topped the list of most-traded wines both by value and volume over the last two weeks. When the wine was released En Primeur in 2022, it was the most affordable of the wine’s last ten vintages.

Since its release in bottle, the wine has seen sustained levels of trading activity on the secondary market. It last traded at GBP 812 (EUR 947) per 12×75, up 15.0% on its release price of GBP 706 (EUR 823) per case.

Champagne’s Rare 2008 was second in both tables. The wine last traded at GBP 1,168 (EUR 1,362) per 12×75, 11.5% below its release price of GBP 1,320 (EUR 1,539) per case.

Two Burgundy wines, Domaine de la Romanée-Conti, Romanée-Conti Grand Cru 2009 and Emmanuel Rouget, Vosne- Romanée Premier Cru Cros Parantoux 2008, were among the most-traded wines by value. Two weeks ago, the 2007 vintage of Rouget’s Cros Parantoux featured on the list.

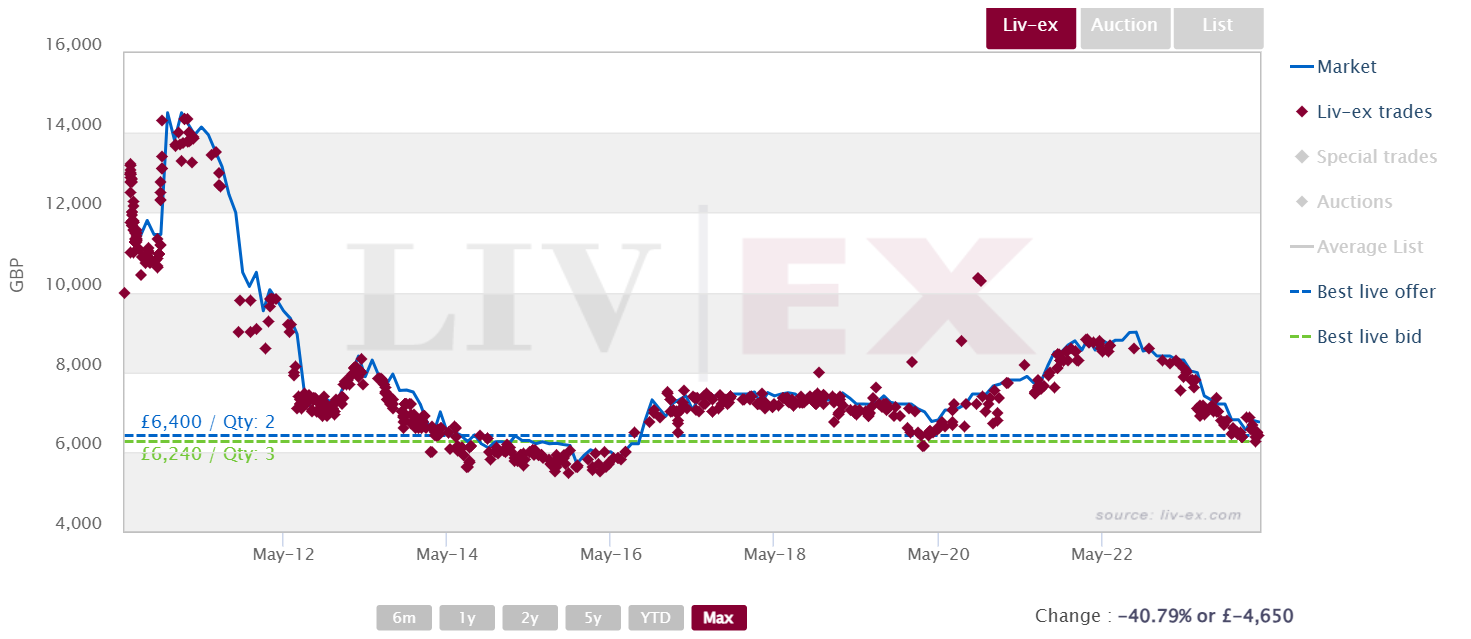

Château Lafite Rothschild 2009 completed the list of most-traded wines by value over the last two weeks. The wine last traded at GBP 6,400 (EUR 7,462) per case. Lafite 2009 has come down 27.3% since its ten-year peak in 2022 and is now back to where it was trading in early 2020 before the most recent fine wine market boom.

Château Lafite Rothschild 2009 trades on Liv-ex

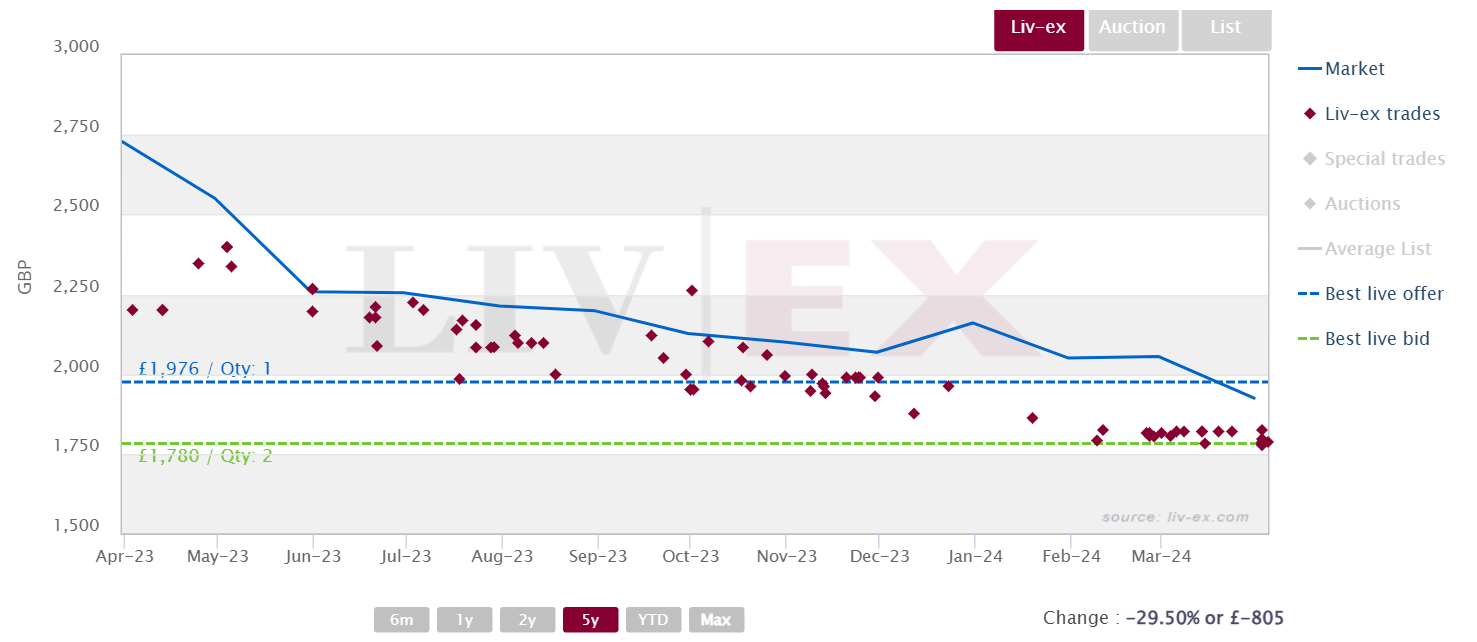

By volume, Louis Roederer’s Cristal 2015, was among the most-traded over the last two weeks. The wine, which was scored 96 points by Antonio Galloni (Vinous) and 96 points by Lisa Perrotti-Brown (The Wine Independent), has been on a downward trend since its release in April 2023. Buyers of Cristal 2015 have been snapping up the wine around the price of the best bid, indicating that sellers are lowering their prices to meet buyers’ expectations.

Louis Roederer Cristal 2015 trades on Liv-ex

Domaines Leflaive’s Mâcon Verzé 2022 was third on the list of most-traded wines by volume and a rosé wine, Domaine Tempier, Provence Bandol Rosé 2022 completed the list, a nod to the start of spring and the warming temperatures in the Northern Hemisphere.

Source: Liv-ex