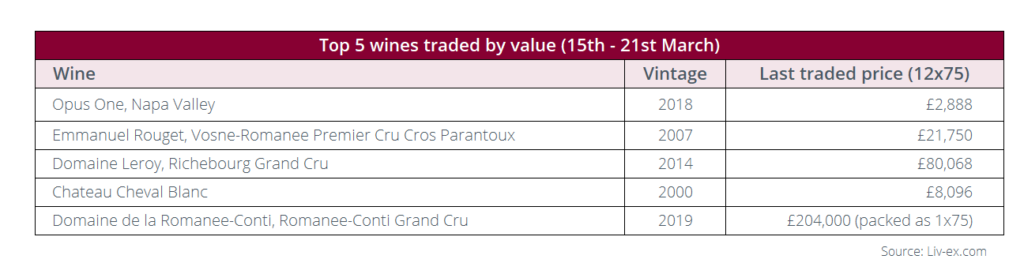

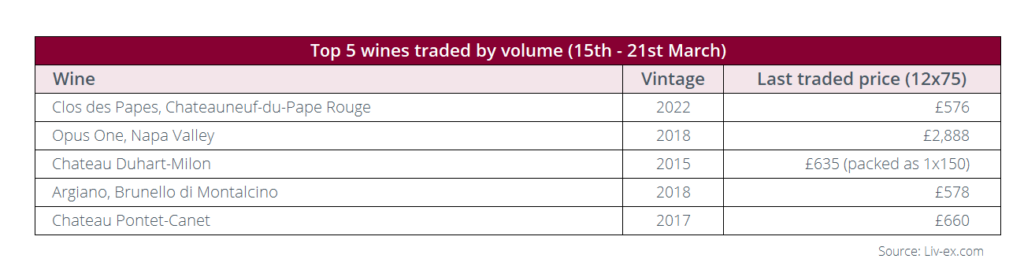

Opus One led weekly trade, followed by wines from Burgundy and Bordeaux. By volume, Clos des Papes led the way.

What’s happening in the secondary market?

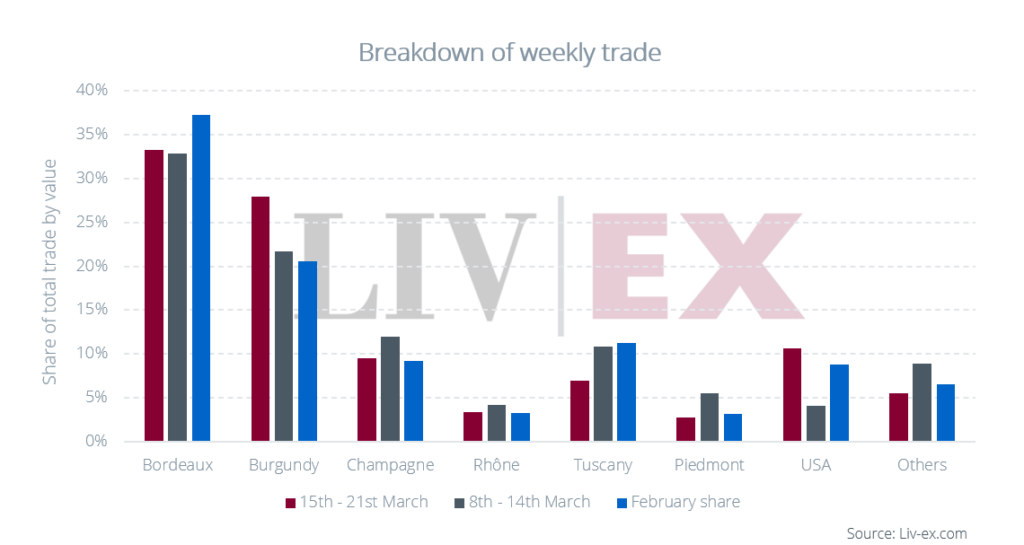

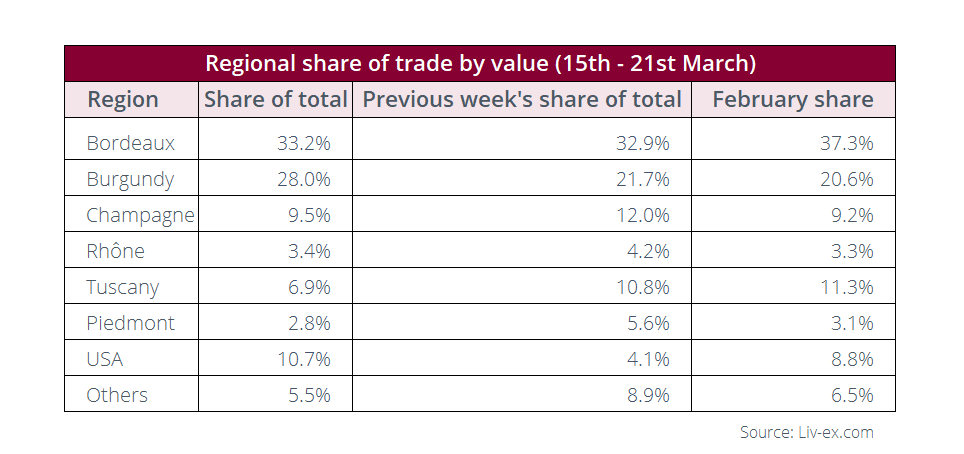

Bordeaux maintained its lead in the market, accounting for 33.2% of total trade by value this week. One of the region’s wines was among the top-traded by value, and two featured on the list of most-traded by volume.

Burgundy wasn’t far behind, holding 28.0% of trade for the last seven days, with three of its wines among the top-traded by value. More on this below.

The USA was one of the winners of the week, its trade share rising from 4.1% to 10.7% of the total this week. Opus One 2018 topped the charts, featuring among both the most traded wines by value and volume.

All other regions saw their trade shares dip week-on-week. Champagne’s share fell to single digits with 9.5% of the total, Piedmont’s halved from 5.6% to 2.8%, Tuscany fell to 6.5% and the ‘Others’ category to 5.5% after two strong weeks.

What were this week’s top-traded wines?

As mentioned above, California’s Opus One 2018 led weekly trade. The wine last traded at GBP 2,888 (EUR 3,359) per 12×75, up 4.6% from its release price of GBP 2,760 (EUR 3,210) per case.

The most-traded wines by value were otherwise dominated by Burgundy, which had three wines among the top five. Alongside Emmanuel Rouget, Vosne-Romanée Premier Cru Cros Parantoux 2007 and Domaine Leroy, Richebourg Grand Cru 2014, three vintages of Domaine de la Romanée-Conti, Romanée-Conti Grand Cru changed hands this week: the 2019, 2014 and 2018.

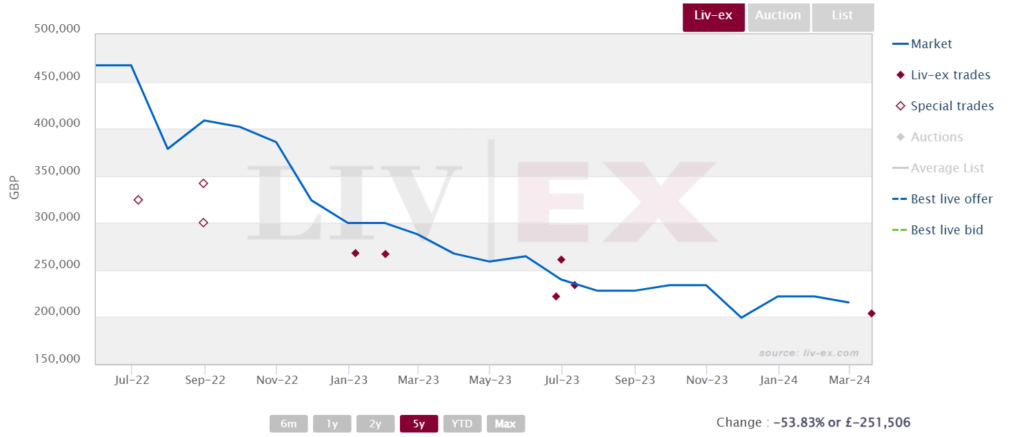

The 2019 vintage has three 100-point scores from William Kelley (The Wine Advocate), Neal Martin (Vinous) and Charles Curtis (Decanter) as well as 99 points from Antonio Galloni (Vinous) and 19.5 from Jancis Robinson. Despite its critical acclaim and brand reputation, the wine has been trading on a downward trend for the last two years.

Domaine de la Romanée-Conti, Romanée-Conti Grand Cru 2019 trades on Liv-ex

Château Cheval Blanc 2000 completed the list of most-traded wines by value. The wine has traded eight times since the start of 2024, culminating in a last trade at GBP 8,096 (EUR 9,417) per case, perhaps reflecting buyers’ renewed appetite for outstanding Bordeaux vintages amid uncertainty in the market.

Bordeaux had two labels among the most-traded by volume, Château Duhart-Milon 2015 and Château Pontet-Canet 2017. The former has seen consistent growth in its Market Price, which currently sits at GBP 650 (EUR 756) per case, up 24.5% from its international release price of GBP 510 (EUR 593) per case.

However, it was the Rhône’s Clos des Papes, Châteauneuf-du-Pape Rouge 2022 which led the way in terms of trade by volume. The wine was released at GBP 732 (EUR 851) per case in November 2023, flat on the 2021’s release price. It last traded 21.1% below that, at GBP 576 (EUR 670) per case.

Argiano’s 2018 Brunello di Montalcino resurfaced among the top-traded wines this week after its success at the end of 2023 following its nomination as the Wine Spectator’s Wine of the Year.

Source: Liv-ex